Equity Insights

In a nutshell

- Reasoning models like DeepSeek R1 mark a shift from traditional predictive models to more advanced ones capable of analysing information, drawing conclusions and solving complex problems

- An evolving AI landscape means beneficiaries are becoming less concentrated and the US no longer holds unchallenged dominance

- While the US remains a leader in foundational AI development, China's engineering optimisations, scale advantages, and commercialisation potential position it as a significant player in the next phase of AI growth

- Most importantly for the next phase of growth, falling costs of AI compute are democratising access to the technology. This trend is expected to unlock higher-value applications and broaden enterprise AI adoption globally

- All of this supports our expectation for software firms to lead the next phase of the AI investment cycle, driving the integration of generative AI into products and solutions

- With very broad technology ecosystems and superapps, emerging Asia presents opportunities for scaling and commercialisation of AI with consumers that are not replicable in developed markets

- Ultimately, the democratisation of AI presents much opportunity for this new technology to fuel earnings growth in emerging Asia and broader emerging markets. This could potentially erode the significant edge in profitability that fuelled historic outperformance by US tech firms over the last decade

Evolution of the AI story

A new AI model originating from China early in the year dramatically lowered the cost of AI compute, placing Chinese companies firmly into the AI value chain and sowing confusion among investors around what comes next.

While much of the volatility in US stock markets this year has been at the hands of trade policy developments, technology stocks initially came under pressure since the late January emergence of new AI models from China. Markets struggled to evaluate the implications, which at once dramatically lowered the cost of compute. The DeepSeek models – comparable to US models but requiring significantly less investment – contain several important breakthroughs around training, inference and how to improve efficiency by optimising the hardware used.

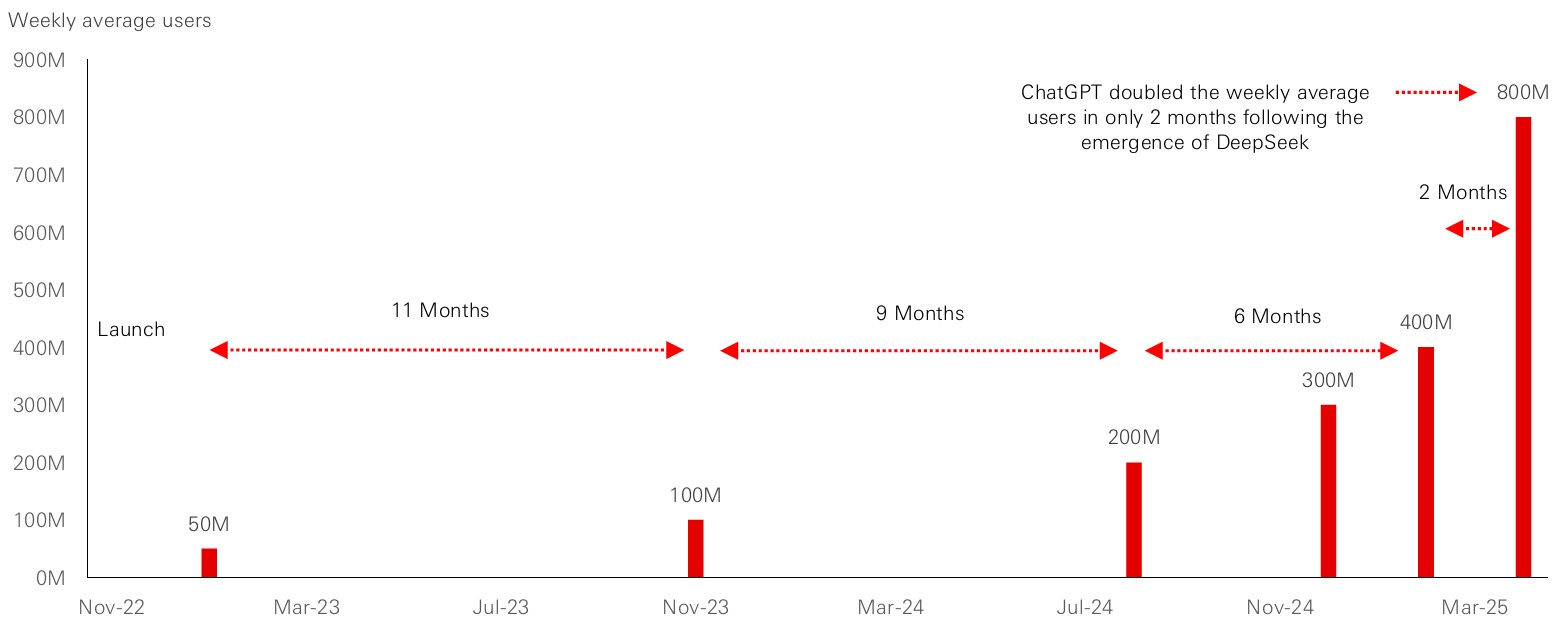

Given the focus on how cheap it had been to train the model, the hundreds of billions of dollars spent on infrastructure and training by the industry was suddenly cast in a negative light, putting ex-China IT stocks under selling pressure. Of course, significant outperformance from parts of the tech sector that fuelled the post-ChatGPT rally came with expectations of continued heavy investment in AI infrastructure. Accordingly, this part of the market was vulnerable to a wobble in confidence. We believe, though, that there are important misconceptions as to the true significance of the model developments. As demonstrated below, the arrival of this new innovation has not dampened interest in the use of existing models.

Figure 1: ChatGPT’s growth has continued to accelerate post-DeepSeek

Click the image to enlarge

Source: Barclays Research, company disclosures, HSBC AM as of April 2025.

DeepSeek’s breakthroughs

While not the only one, DeepSeek’s R1 model represents a shift from traditional predictive LLMs that provide answers based on pre-existing data, to reasoning models that can analyse information, draw conclusions, and generate solutions to complex problems. This capability is akin to human reasoning, where individuals assess situations, consider various factors and arrive at informed decisions. For example, when posed with a question a traditional model might provide an immediate answer based on its training data. In contrast, a reasoning model breaks the question down into components, evaluates the information and arrives at a more accurate conclusion. This iterative process enhances the quality of the answers generated, making reasoning models particularly valuable in complex scenarios.

The ability to reason is essential for AI systems to operate effectively in real-world situations. In enterprise settings, reasoning models can streamline processes such as onboarding of new employees for instance, facilitating an AI agent capable of interacting with various systems to action relevant steps (i.e. issue access pass, procure relevant laptop type, etc.). Of course, the potential goes beyond this. By automating tasks and making informed decisions based on available data, these models reduce friction and enhance operational efficiency.

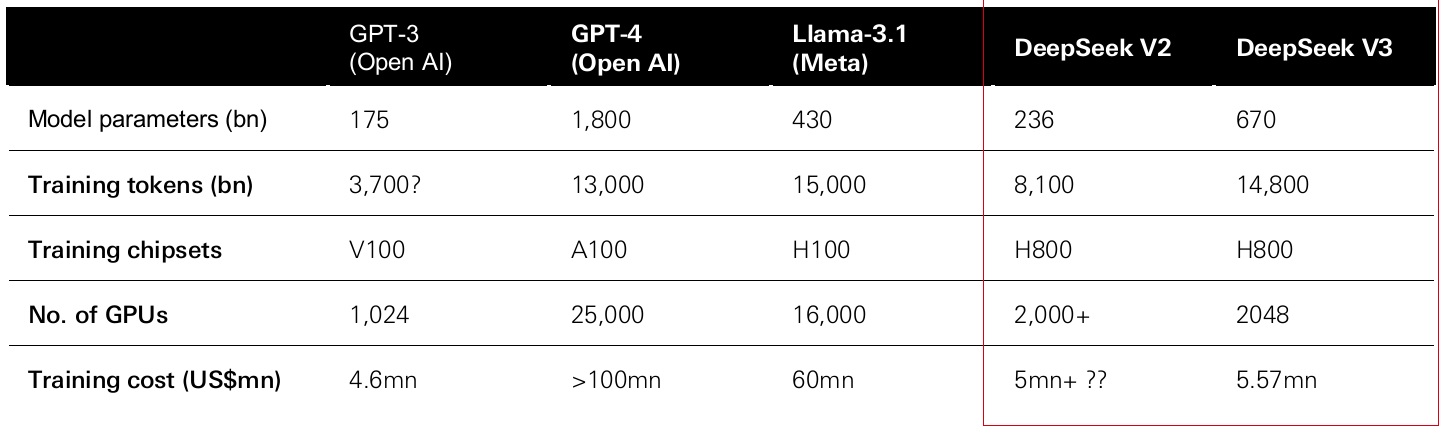

Yet, DeepSeek’s real ingenuity lies in engineering optimisations that reduce AI compute costs while maintaining performance. This has been made possible through architectural innovations such as Mixture of Experts (MoE), Multi-Head Latent Attention (MLA), and unique communication protocols enabling high efficiency even on lower performance chips like the Nvidia H800 that was permissible for export to China.

In terms of impact going forward, DeepSeek has open-sourced its work, democratising access to cutting-edge reasoning models and empowering developers globally to iterate, adapt, and deploy AI at scale. This will be helpful in enhancing the technology and addressing issues such as AI ‘hallucinations’. Greater accessibility should also translate to more businesses leveraging the value of these models, supporting more demand-driven investments, fuelling further innovation and growth that could be instrumental in reducing inference costs.

OpenAI has also launched reasoning models but had essentially kept the process closed. This changed post-DeepSeek, with the subsequent promise of an open-source model to be released in the coming months – signifying a competitive shift that supports accessibility and creates beneficiaries down the AI supply chain.

Figure 2: Resources for training of models

Click the image to enlarge

Source: HSBC AM, company data. April 2025

The cost of AI: misconceptions and realignment

The launch of DeepSeek’s R1 garnered significant attention due to its widely-circulated figure of $5.5 million in training costs. For many reasons we think this underestimates the full investment and misses the point. The lasting impact is the release of important breakthroughs to the model community that could substantially lower the cost of inference and thus accelerate AI adoption.

One improvement employed by DeepSeek is how the algorithms work and how data is used. Using specific, very targeted chunks of data to generate answers vastly improves efficiency, speeding up cost reduction in these models.

Today, inference costs are declining by 10x annually on average. Reflecting the classic Jevons Paradox (i.e. as compute becomes cheaper and more efficient, consumption increases), a rise in consumption going forward should be due to:

- Increased user base (hundreds of millions using LLMs daily),

- More time spent per session (more complex reasoning),

- More compute per request

Lowering the cost of inference — the process of generating reasoning from AI models — speeds all of this. While a reasoning model will solve a complex task more accurately, it can require 150x more compute than a basic LLM, per an example shared by Nvidia’s CEO Jensen Huang at their recent GPU Technology Conference. This is as much as 400 times that of a standard Google search.

The trajectory of hardware development should also support the path to cost reduction. Nvidia’s new Blackwell and upcoming Rubens GPUs are expected to significantly reduce the total cost of ownership for inference operations. As these hardware advancements come to market over the next two years, reasoning models will become more accessible and scalable, unlocking higher-value applications and broadening enterprise AI adoption.

This is a net positive for the entire AI value chain, including hyperscalers, infrastructure providers and emerging software leaders who are positioned to benefit from the broader deployment of generative AI models.

In the short term, lower cost of compute should benefit the software sector relative to the semiconductor sector. As the software sector invests and integrates Generative AI into their products, inference is an operating cost to them – anything that can reduce this will be welcomed. This shift has started to be reflected in equity returns, with a rotation away from massive semiconductor outperformance generated in the initial post-ChatGPT rally.

In the context of previous platform shifts such as the mobile-internet cycle, while the semiconductor industry has been the primary benefactor from a flood of investment to date, the impact on the software sector is still in its early stages. Our view remains that substantial lowering of the cost of compute is a necessary condition for a move to the next stage of the investment cycle to take place.

For the hyperscalers and infrastructure providers, the impact becomes nuanced. Some have continued with their platform approach, allowing models to reside on their infrastructure, thus monetising usage and inference. Others have developed their own models as well as their own compute for internal purposes. Rapid advancements and commoditisation of compute is more likely to be a headwind for the latter approach and a tailwind for the former.

China joins the AI investment story

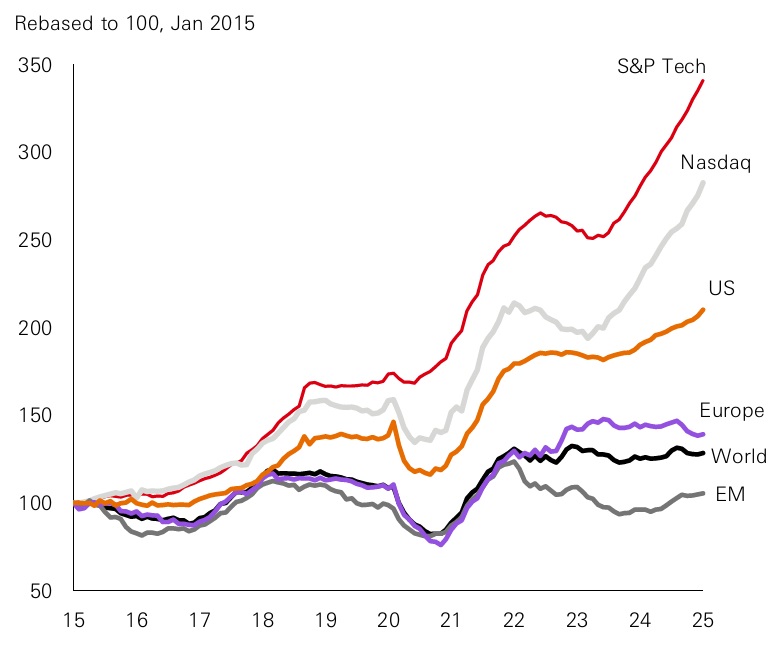

Up to now, the US has dominated the AI revolution, benefiting from deep capital markets, first-mover advantages, and robust ecosystems. Massive profitability of US tech firms has also supported investment in the technology. As of 2024, Nasdaq profits were four times the global average. However, that gap is now narrowing and brings regional broadening into consideration as part of the next stage of the investment cycle.

Today, US tech capex-to-sales ratios are above levels seen in the 2000 dot-com bubble. If those massive capital investments don't yield proportionate revenue growth, margins may compress and valuations reset. This could further this year’s reallocation of global capital towards underrepresented regions which aligns with our investment outlook of markets and economies ‘spinning around’.

China may not have led in foundational AI innovation, but their engineering prowess, scale advantages through superapps, and potentially easier path to commercialisation position them as major beneficiaries of the next wave of AI development. Amidst the rally in China technology stocks post-DeepSeek, this rerating still leaves China large cap tech at roughly half the price of US large cap tech relative to earnings. Accordingly, if monetisation and growth is realised, there is ample room for further rerating.

Although US companies are still leading globally in terms of original innovations, we believe China could lead globally in terms of engineering optimisations, production and commercialisation at scale. This creates a large growth runway for China’s internet/cloud platforms, where consumer-facing LLM-powered applications can lead to improving monetisation and cost.

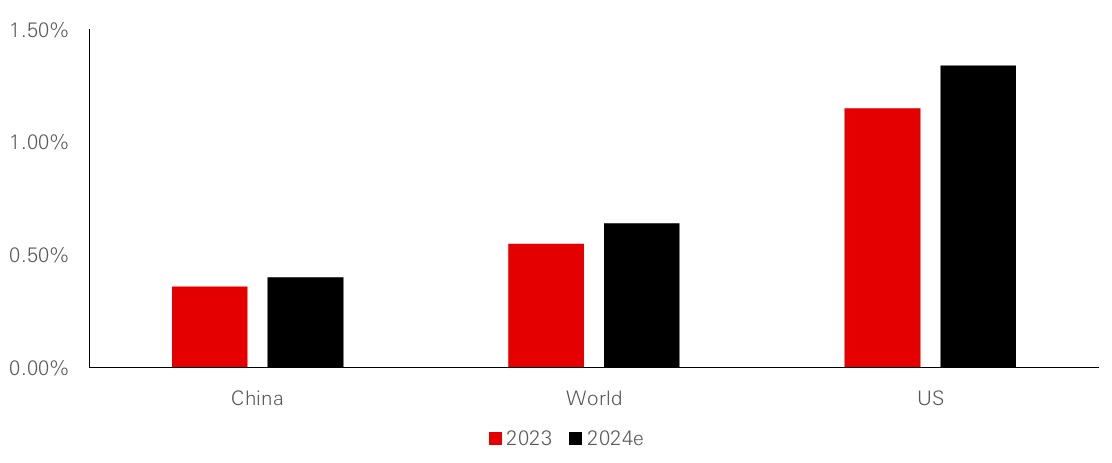

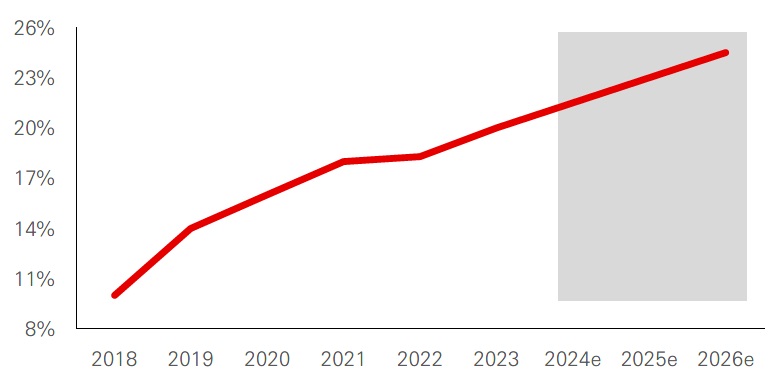

Figure 3: We are in early stages of growth in China cloud spend (Cloud spend as per cent of GDP)

Click the image to enlarge

Source: Statista, Gartner, HSBC Research estimates. March 2025.

Demand for AI-driven solutions in China has surged this year since the release of DeepSeek. In conjunction, the use of open-source AI is paving the way for faster application development and innovation, presenting clear opportunities for independent AI application developers.

As early beneficiaries, the leading cloud providers are integrating DeepSeek R1-like models into their cloud infrastructure, creating new value propositions while enhancing operational efficiencies. Meanwhile, growing AI adoption creates beneficiaries down the local supply chain, with local hardware manufacturers and software developers filling gaps created by US export restrictions.

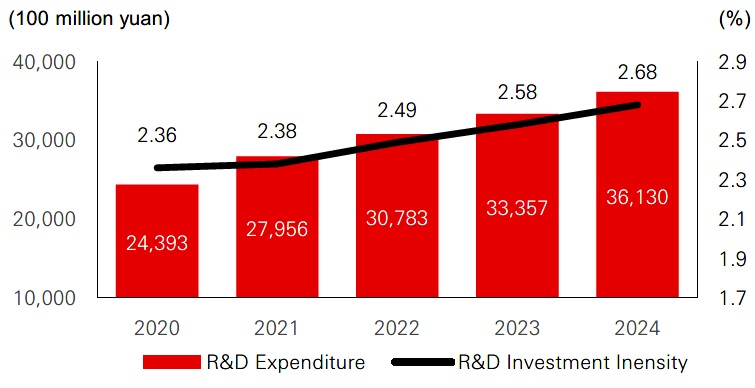

Figure 4: China’s tech investment supports local advances

Click the image to enlarge

Source: National Bureau of Statistics of China, as of 24 January 2025.

Figure 5: China semiconductor self-sufficiency

Click the image to enlarge

Source: Gartner, WSTS, Morgan Stanley Research estimates, February 2025

As AI use cases grow, the demand for customised and locally manufactured compute components is expected to rise. Furthermore, proliferation of AI-enabled applications on consumer devices is likely to shorten upgrade cycles, creating a favourable environment for hardware providers and component suppliers alike.

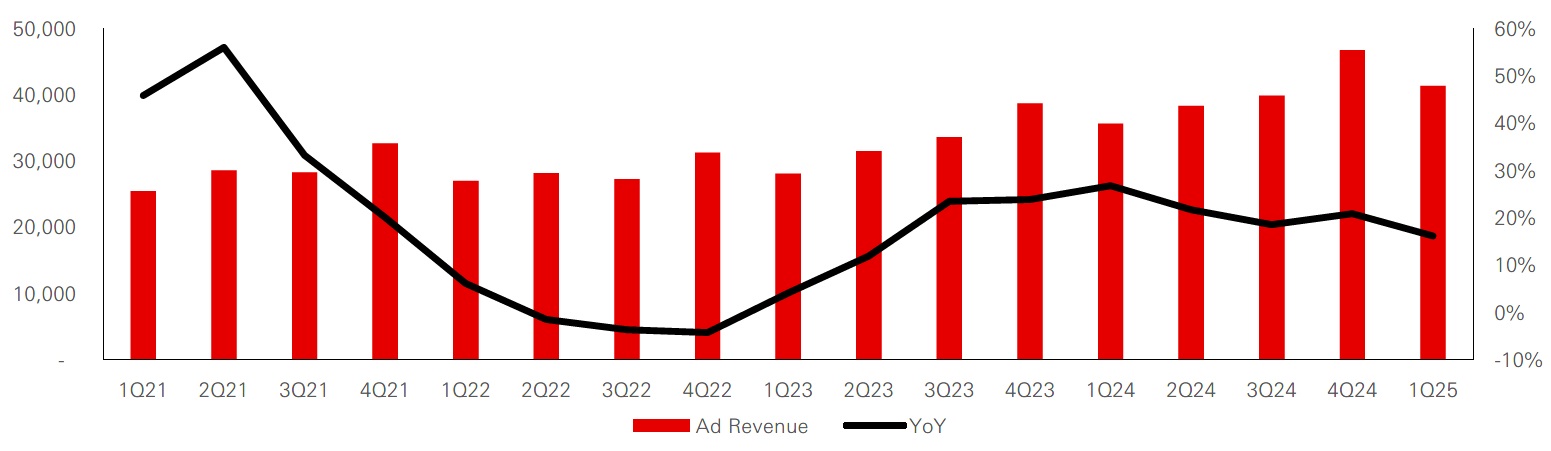

Ultimately, the value of AI model developments lies in how businesses use AI to improve their existing products and services over time. We can look to Meta as an example of how AI has already been monetised within a large consumer platform. Leveraging AI, Meta has automated much of its advertising process in the past two years. Advertisers can now use AI to generate ad content and develop advertising strategies that outperform human efforts. Further benefits include an AI-powered matching system that ensures a better advertising targeting rate.

Figure 6: Meta’s advertising revenue and y-o-y growth (USDm)

Click the image to enlarge

Source: HSBC Research, Company data, HSBC AM, March 2025.

With the help of DeepSeek, Chinese internet platforms are looking to implement similar improvements to their business models, with potential for ever larger impact thanks to their massive ecosystems. Over time, this could evolve into full-fledged AI agents capable of delivering advanced solutions across different domains. Vertical internet players such as online healthcare, education and travel platforms are also leveraging AI for personalized consulting services, creating new value proposition for consumers.

Beyond internet companies, a broad swathe of industries are becoming fast movers in integrating large language models into their operations. Likewise, government institutions are integrating AI, supporting expected growth in private AI cloud projects for state owned enterprises and government agencies.

Beneficiaries of growing AI adoption extend further into emerging Asia

Superapps in Asia can seamlessly facilitate the monetisation of AI functionality with consumers, presenting an opportunity that is not replicable in developed markets. As AI is integrated across these large platforms, enhancements should include more targeted advertising to a very broad user base, better e-commerce experiences for these consumers, and more efficient generation of entertainment content including games (allowing greater production of differentiated content for consumption). This supports the promise of AI leverage in Asia picking up steam and supporting earnings growth as the cost of compute continues to reduce.

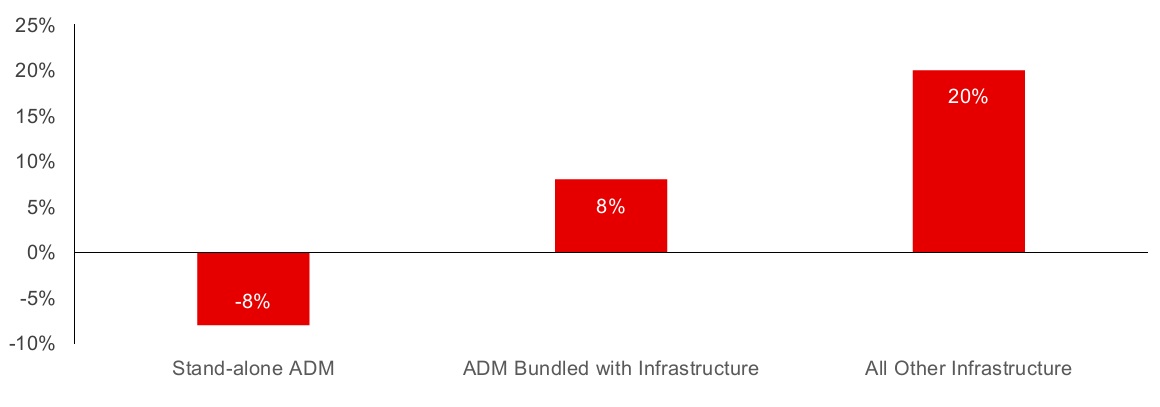

Separately, as lower cost of compute drives greater enterprise adoption of generative AI globally, India becomes an interesting beneficiary for its own reasons. Commonly dubbed as ‘the world’s back office’, a large part of India’s technology sector consists of IT services. As system integrators, they stand to benefit from large scale adoption of Gen AI across enterprises.

Currently, global enterprise adoption is still transitioning from proof of concepts to larger scale adoptions as use cases evolve. Consulting services providers incorporating AI solutions, like Accenture, TCS and Infosys, have spoken about Gen AI gaining scale in their orderbooks. However, it is not at the core of offerings, still primarily focused on enhancing skills, capabilities and reskilling of employees – it largely remains on the periphery of solutions rather than a core driver.

At the same time as spending on AI infrastructure – data processing and storage – has progressed at a rapid pace, there has been a slowdown in spend on Indian IT services over the last year. This points to spend on AI buildout consuming budgets, leaving smaller slices of the pie for IT Services. Even the hyperscalers, with their near limitless budgets, have cut IT services spends as they have grown their substantial AI infrastructure capex. Figure 4 reflects this disparity in spend for stand-alone application development and maintenance services versus infrastructure spend globally.

Figure 7: 2024 Growth in ADM services

Click the image to enlarge

Source: Information Services Group Index, January 2025.

While DeepSeek may not be adopted in the west, the ideas around optimisation and doing more with less will certainly permeate US tech. This means the cost of adoption will continue to come down and more domain specific LLMs will likely be developed. Here, Indian IT can participate in optimising LLMs, even with lower processing power. Provided the US macro environment supports continued corporate spending ahead, we expect a revival of discretionary spending for Indian IT Services as the Gen AI story evolves.

What comes next

DeepSeek’s rise has muddled the AI investment narrative and marked a turning point in certain ways. Yet, such developments in the technology are to be expected, and per Jevons Paradox, only contribute to the ultimate conclusion of AI’s reach expanding across companies and consumers worldwide.

With reasoning models now in the hands of billions, the AI race is no longer just about who builds the smartest machine, but who gets it into the most hands at the lowest cost. And while the US remains the leader in foundational AI development, its unchallenged dominance is fading.

In the long arc of technological revolutions—from steam to silicon to intelligence— the winners are those who adapt, scale, and distribute. We see several implications for equity portfolios. In terms of market segments, we continue to believe that software firms will lead the next stage of the investment cycle. It is this segment that must facilitate the delivery and use of AI both in enterprises and with consumers, as declining compute costs expand the opportunity set for software solutions.

Nonetheless, much investment is still needed in the hardware to achieve the desired model capabilities and efficiencies. Accordingly, a long growth runway for high-performance GPU chips that have powered the AI revolution remain, along with the less powerful but more flexible ASIC chips whose functionality may become more useful as model efficiencies increase and use cases expand.

Regionally, we anticipate that emerging Asia will gain greater investor attention. With the launch of the DeepSeek models broadening and accelerating access to leading AI capabilities, adoption in these markets is supported by inherent advantages in monetising the technology. And as the cost of compute declines, operational gains and enhanced product and service offerings should feed through to earnings growth in these markets. Accordingly, we could see the significant edge in profitability that fuelled historic outperformance by US tech firms over the last decade begin to erode.

Figure 8: Net profit growth over a decade

Click the image to enlarge

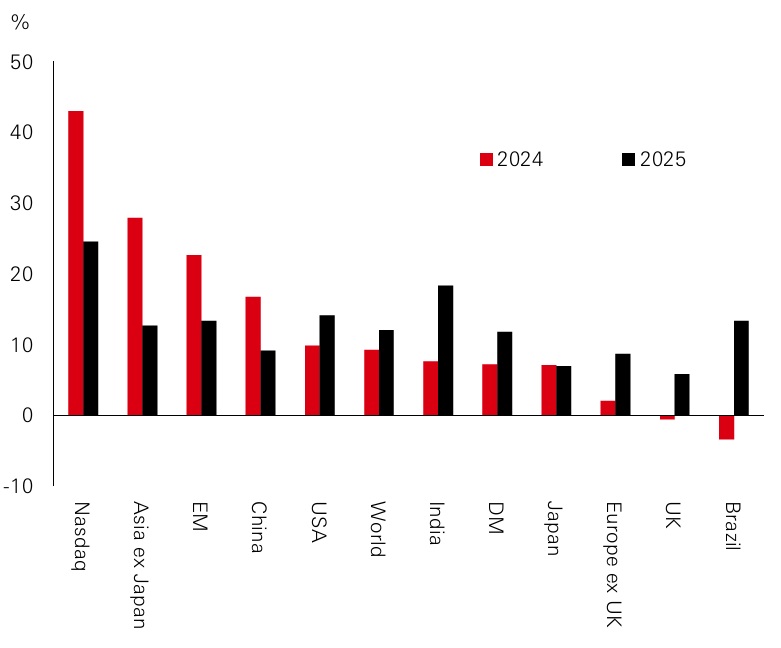

Figure 9: Consensus EPS growth (IBES) - Nasdaq from 4x to 2x world growth in 2025e

Click the image to enlarge

Source: Refintiv, Datastream, MSCI, HSBC AM, March 2025.

For informational purposes only and should not be construed as a recommendation to invest in the specific country, product, strategy, sector or security. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.