Middle Eastern Conflict and Implications for Asian Energy Policy

Executive Summary

Asia, including developed markets such as Japan and Korea, is hit hardest by the Middle East energy supply shock as Hormuz flows have largely ceased. ~90 per cent of exports were Asia-bound, and Platts Dubai/Oman now trades at a 10–20 per cent premium to Brent/WTI.

Near-term stabilization is coming from buffers and stopgaps, but the strategic direction is an accelerated energy transition, given attractive economics, faster deployment, and national resiliency imperative.

The Middle Eastern conflict is “serving as a significant turning point … [there is] a growing national consensus that we must undergo a fundamental energy transition.

Introduction

The current conflict in the Middle East has precipitated an energy shock not seen since the 1970s – one that disproportionately affects Asia, the end destination for the majority of oil and gas products from the Gulf. This energy shock will have significant implications for short term energy prices and medium-long term energy policy. Whereas the 1970s playbook emphasised demand dampening, stockpiling, and supply substitution, governments in 2026 are better prepared. They are looking to the medium-long term, for energy supplies that are insulated from volatility in global oil and gas markets – renewables.

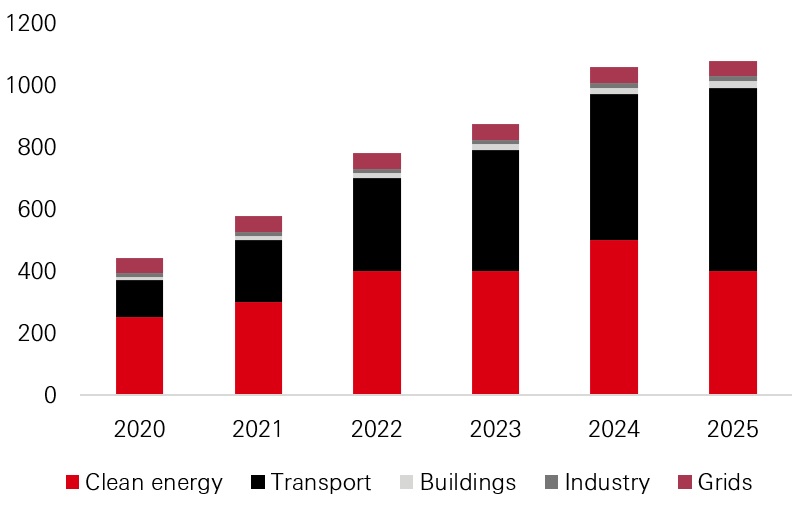

Developed Asia’s energy transition, from fossil-fuel dependency to renewable and low carbon supplies, is well underway already, with a record USD 1.1tn of investment in 2025,1 and favourable economics are driving deployment at scale, backed primarily by government and private sector decarbonisation commitments. We see the current Middle East conflict as an additional catalyst for this already fast-growing sector, and as a significant opportunity for investors.

Asia Pacific energy transition investment (USD, bn)

Click image to enlarge

Figure 1 Source: BNEF, March 2026

The scale of the disruption

The Strait of Hormuz is the aorta of the global oil and gas system – roughly 20 per cent of global petroleum liquids consumption and a fifth of global seaborne gas transited the Strait pre-war, which has almost entirely ceased.2 The conflict is the most serious energy shock in global history, exceeding the 1970s’ shocks in the impact on supply. Even in a scenario where hostilities cease rapidly, the region has already sustained significant damage to energy infrastructure. The full extent remains uncertain, but the implication is clear: restoration of pre-war export capacity is unlikely to be immediate, and disruption is likely to continue.

The direct impact falls predominantly on Asia, which is the principal destination market for gulf exports. The IEA estimates that almost 90 per cent of total Hormuz export volumes in 2025 were destined for Asian buyers and many Asian refineries are configured for Gulf crude, limiting their ability to substitute.3 Platts Dubai and Oman, the primary benchmarks for Asian oil, are at a 10-20 per cent premium over Brent or WTI, reflecting the tighter supply facing the region. Gulf LNG is similarly an important energy source for the region - Singapore, for instance which generates 95 per cent of its electricity from LNG, of which c. 45 per cent comes from Qatar alone.4 As such, the region is uniquely vulnerable, and governments have strong incentives to reduce reliance on this volatile energy source and instead develop more resilient energy infrastructure.

The 1970s shocks

Of course, this is not the first shock that the region is facing. Japan’s response to the 1970s crises provides a useful reference for the impact these shocks can have, with responses focused on ensuring both short-term stabilisation and longer-term structural change:

- Stockpiling: Passed the 1975 Oil Stockpiling Law, which mandated significant oil and gas reserves in order to ensure a stable supply in times of crisis

- Energy efficiency: Sponsored energy efficiency programmes, such as the 1978 Moonlight Program, which focused on power generation, heat utilisation, and power storage technologies

- Renewables: Sponsored research and development of renewable energy sources to eliminate their reliance on foreign energy sources, including as part of the 1974 Sunshine Project - ultimately unsuccessful at the time

- Alternative fuel supplies: Diversified fuel supplies to limit the importance of any one source of fuel, which was more successful

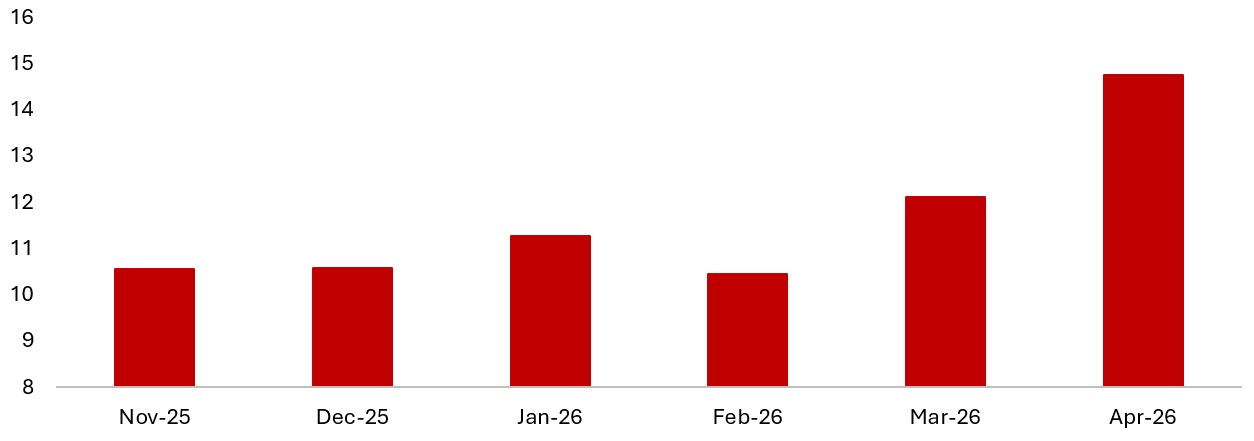

JPEX Day Ahead Market Prices (JPY/kWh)

Click image to enlarge

Figure 2 Source: Japanese Government, December 2024

Responses in 2026

Developed Asian nations are better prepared in 2026 than they were in the 1970s. Oil and gas stockpiles sat around 180 days before the conflict, and they provide a buffer in the near term. Governments also have alternative fuel sources they can turn to in the short term, including by lifting restrictions on coal power generation temporarily, such as is happening for decommissioned coal-fired powerplants in South Korea, Thailand, and Japan. Again, these are short term measures - any new coal-fired powerplants risk becoming stranded assets, as cheaper and cleaner forms of energy take their place, particularly in light of national transition policy frameworks.

Even with these measures in place, energy prices have still risen materially in places like Japan. This is not just in merchant wholesale prices, but generation companies on the ground have also reported immediate upwards pressure on long term power purchase agreement (PPA) pricing for solar projects, for example.

JPEX Day Ahead Market Prices (JPY/kWh)

Click image to enlarge

Figure 3 Source: JPEX, April 2026

The Asian Energy Transition

The biggest difference between the policy responses in 1973/9 and 2026 is that energy transition technologies have matured, and we foresee the primary policy response in the form of an acceleration in the energy transition in Asia. Renewables are an attractive proposition for policymakers increasingly worried about national resilience, as a form of generation capacity divorced from volatility in oil and gas markets. South Korea’s administration has been most explicit in spelling out the political and strategic rationale. Kim Sung-hwan, the Minister of Climate, Energy and Environment framed accelerated renewable deployment as a direct response to the Middle East conflict, stating that the crisis represents "a growing national consensus that we must undergo a fundamental energy transition".5

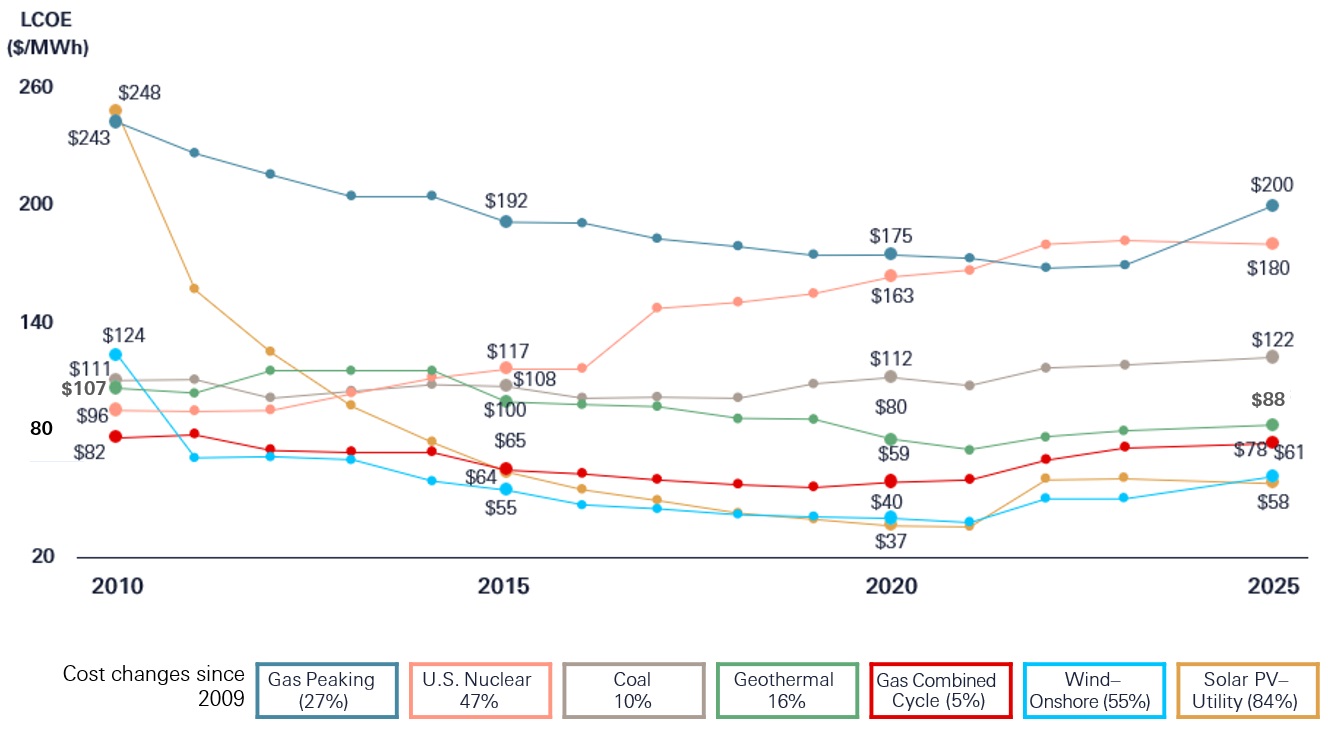

The source of much of the momentum behind the energy transition, even before the conflict began and the price of oil and gas rose precipitously, was the attractive economic rationale. PV+BESS already enjoyed a LCOE advantage (USD 50-131/MWh) over gas peaking (USD149-251/MWh), nuclear (USD 141-220/MWh), and coal (USD 71-173/MWh) generation in many markets.6 Underlying this is a sustained decline in technology costs, with Solar PV production costs, for instance, having fallen by more than 90 per cent over the past decade with further reductions expected. Similarly, the cost of batteries, which are of critical importance to connect to electric grids to help manage the intermittent renewable power supply, have fallen by more than 92 per cent over the last 15 years.7

Levelised Cost of Energy (LCOE) Comparison: Significant historical cost declines for utility-scale renewable energy generation technologies

Click image to enlarge

Figure 4 Source: Lazard, June 2025

Renewable power sources also enjoy an advantage in the speed of construction. Development cycles for large-scale solar are typically 3-5 years, lower than nuclear (10-15 years) or fossil fuels (5-7 years). Smaller-scale, distributed solar is even faster. For governments looking to quickly bring capacity online, as well as investors looking to minimise development risk, these are attractive characteristics.

Conclusion

The supply shock is significant, but the second-order effects on policy and capital allocation are equally important over the long-term. The conflict has highlighted the fragility of the seaborne energy trade through maritime chokepoints. These vulnerabilities will remain salient in infrastructure investment decisions, forcing policymakers to ask the question – can they rely on a consistent supply of oil and gas in times of crisis?

Against this backdrop, we believe that the Asian Energy Transition offers significant opportunities for investors. In the short term, we are already observing PPA prices rising for renewable energy generation capacity. Longer term, existing demand drivers we’ve discussed in previous papers, improving economics, and the new additional impetus created by the Middle East conflict will further strengthen the investment case for the sector.

1) Source: BNEF, March 2026

2) Source: IEA, February 2026

3) Source: IEA, December 2025

4) Source: Singapore Government Ministry of Trade and Industry, KPLER, December 2025

5) Source: CNBC, March 2026

6) Source: Lazard, June 2025

7) Source: BNEF, December 2025

Important Information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation, and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets. Investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agengy;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D070155_v1.0; Expiry Date: 30.04.2027