Multi-Asset Insights

In a nutshell

- There is no single evergreen hedge for equity tail risk; the defensive behaviour of bonds, FX, commodities and options is highly regime dependent and shaped by growth-inflation dynamics, the origin of shocks, fiscal conditions and market structure

- Government bonds hedge equities effectively when the stock bond correlation is negative and bond specific risks are low. Rising real rates, higher inflation variance and elevated fiscal uncertainty can push correlations positive and weaken their safe haven role

- Within risk assets, diversification is increasingly found through sectors, factors and options rather than simple regional splits, with defensive sectors and tailored option overlays helping to reduce drawdowns when correlations spike

- Effective tail risk management now calls for a dynamic, regime based framework that blends sovereign bonds, alternatives, FX, commodities and options, rather than relying on any single static safe haven

Rethinking safe havens for equity tail risk

Defensive assets are back in focus, but the behaviour of potential safe havens is strongly conditioned by macro regimes, crisis origins and market structure.

Harry Markowitz, the Nobel prize winning US economist and pioneer of Modern Portfolio Theory, once famously said that “diversification is the only free lunch”. If we do not have perfect knowledge of future returns, an investor can reduce overall portfolio risk without sacrificing potential returns by diversifying their portfolio.

But even well diversified portfolios can still carry significant risk. Historically, globally diversified portfolios containing only equities have seen stretches of more than 20 years of negative real returns, while similar bond only portfolios have in some cases faced multi decade real wealth destruction, particularly around major wars and inflationary episodes. The risks associated with these portfolios are still lower than investing in a single stock or bond, but they remain considerable nonetheless.

When thinking about diversification, we tend to focus on building portfolios with more than one asset class – the 60/40 portfolio of stocks and bonds being the classic example. The idea hinges on combining uncorrelated (or negatively correlated) assets to achieve the “free lunch” Markowitz described.

However, asset class dynamics mean this hasn’t always been easy to do, particularly during macro shocks. Even the 60/40 portfolio suffered deep drawdowns in systemic crises such as the First World War and the Great Depression, underlining that simple diversification is not a guarantee against large losses when macro shocks are severe.

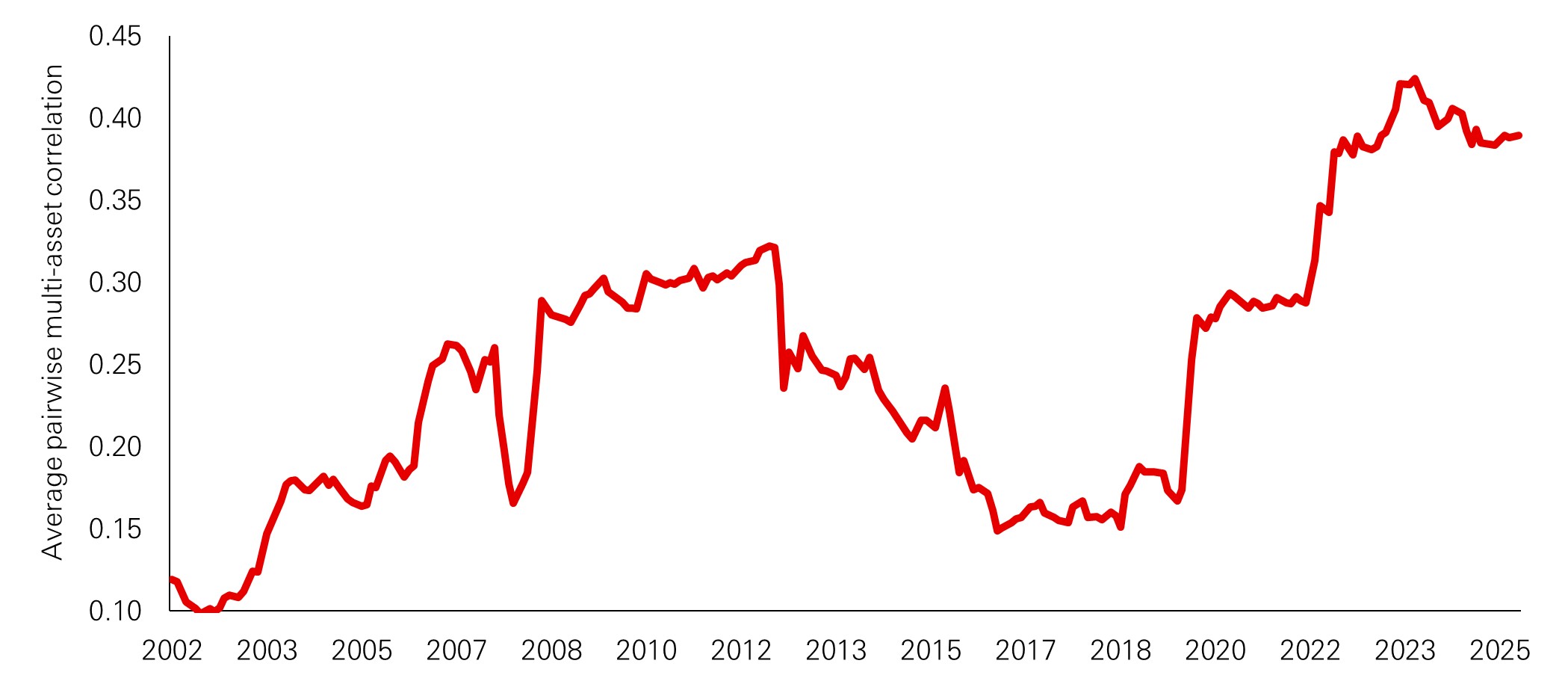

Over recent years, average correlations within multi-asset portfolios have trended higher as markets have become more globally integrated. Against this backdrop, defensive assets are back in focus, but historical evidence suggests there is no evergreen hedge for equity tail risk. Instead, the behaviour of potential safe havens is strongly conditioned by macro regimes, crisis origins and market structure.

Figure 1: Multi-asset correlations have risen

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg. Data as of March 2026.

Fixed income and the importance of the stock-bond correlation

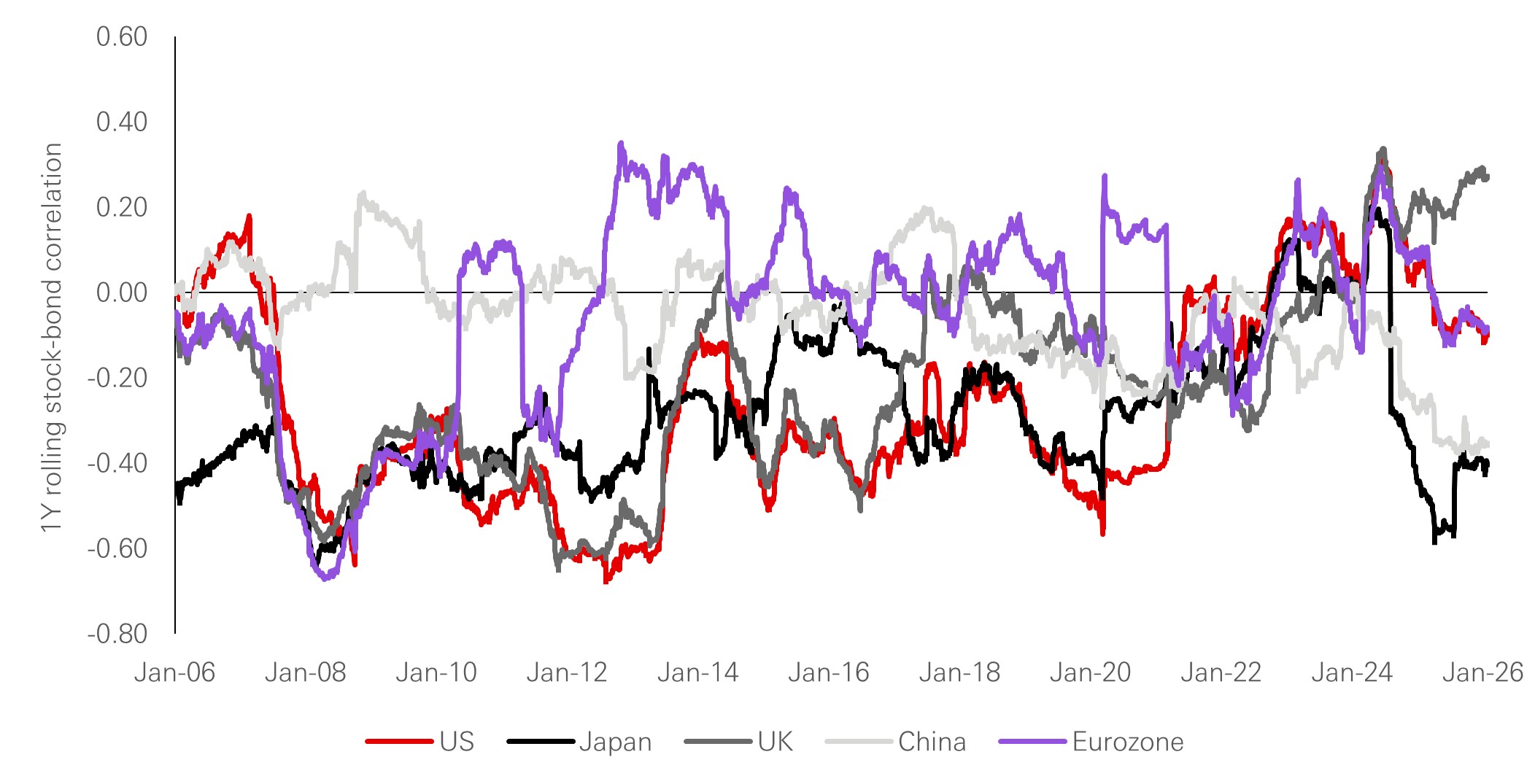

Government bonds have been the default hedge for equity risk, but their effectiveness is fundamentally tied to the stock‑bond correlation (SBC). When correlations are negative and bond‑specific risk is low, sovereign bonds can effectively exhibit a negative risk premium, behaving as defensive assets and thus providing an effective equity hedge.

The SBC is dynamic, and historically a positive SBC has been the most persistent regime over time. SBCs also vary between economies. For example, the negative correlation exhibited between 2000 and 2020 was mostly limited to North America, whereas in Europe it had already reversed during the European sovereign debt crisis, led by periphery countries and later joined by core European nations.

Figure 2: Different economies = different behaviour of SBC

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg. Data as of March 2026.

This divergence is an example of how macro conditions play a central role in determining SBC, and thus the suitability of bonds as a diversifying or safe haven asset. Rising real rates and higher inflation variance relative to growth variance tend to push SBC higher, as both equities and bonds sell off in response to inflation or policy shocks. By contrast, rising growth risks, increased risk aversion, flight‑to‑quality flows and more accommodative monetary policy tend to pull SBC lower, as bonds rally when equities fall.

The origin of the shock matters a great deal in this respect. Trade and tariff shocks have historically seen sovereign bonds perform relatively well in equity drawdowns, as growth concerns dominate the potential inflation impacts. By contrast, periods of elevated military spending often involve shifting part of the fiscal burden onto bondholders through surprise inflation and financial repression, leading to weak real bond performance even as risk assets sell off.

Recent history has highlighted an additional layer: market microstructure. During the early phase of the Covid pandemic, US Treasuries briefly sold off alongside equities as dealer balance sheet constraints and forced liquidations overwhelmed safe haven flows, showing that even benchmark sovereigns can experience pro‑cyclical price action when intermediation capacity is strained.

In environments where the SBC is positive and fiscal uncertainty elevated, alternative strategies have historically played a larger role, including commodity carry, credit carry and bond trend‑following, which has delivered strong returns at near‑zero correlation to 60/40 portfolios and tended to outperform in inflationary periods.

Rate and credit derivatives – such as CDS index protection buyers and receiver swaptions – can also provide targeted hedges to shifts in policy expectations and credit spreads when duration is less reliable as a defensive tool.

Looking ahead, several indicators are relevant for assessing the appropriateness of sovereign bonds as hedges. These include net debt‑to‑GDP, defence‑spending trends, measures of market liquidity and other components of the convenience yield on benchmark sovereign bonds. The supply and demand backdrop is another consideration as government borrowing has crept higher in a number of countries, an effect that may be further exacerbated if geopolitical tensions escalate.

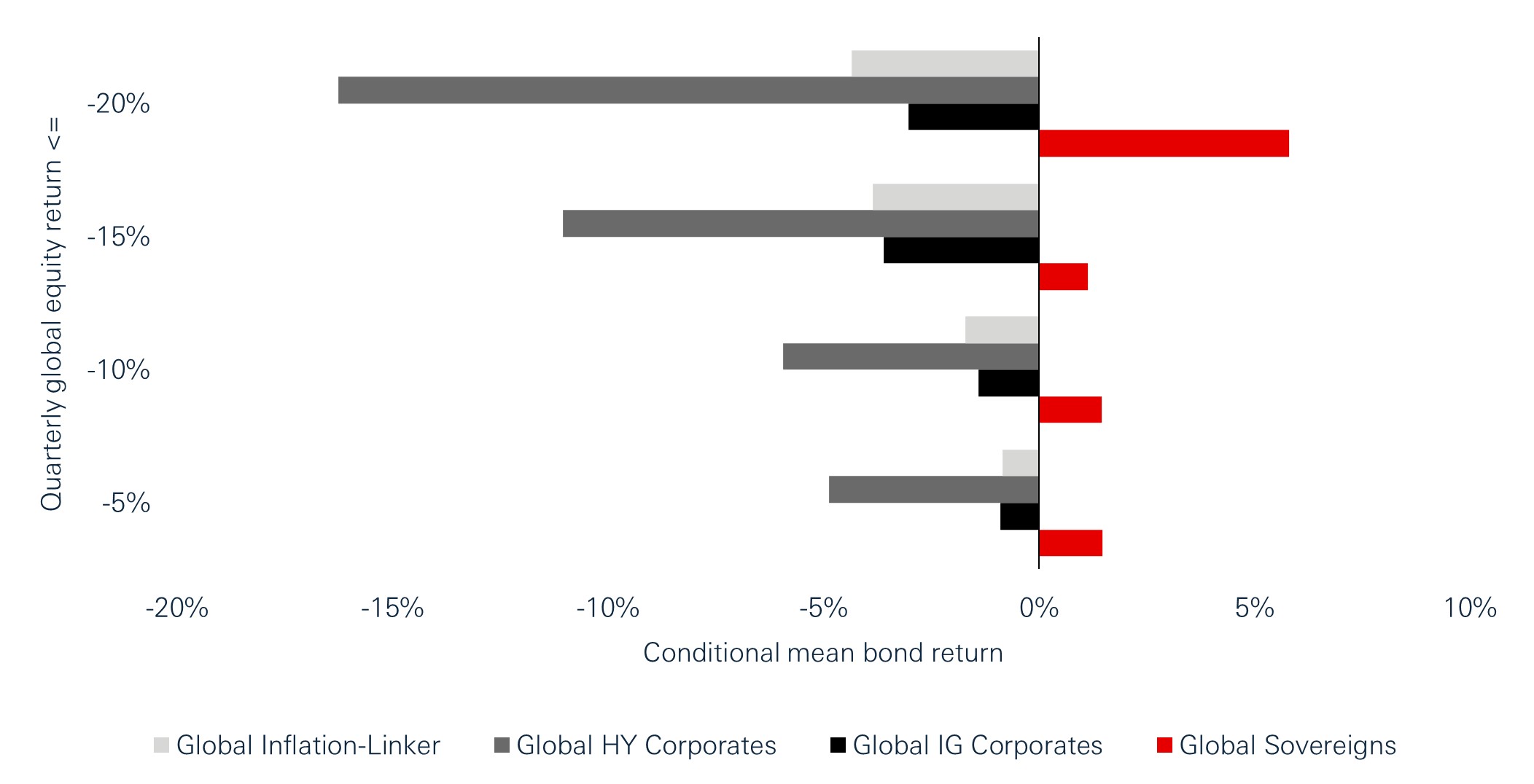

Figure 3: Nominal sovereign bonds can be a safe-haven

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg. Data as of March 2026.

Look to sectors for equity diversification

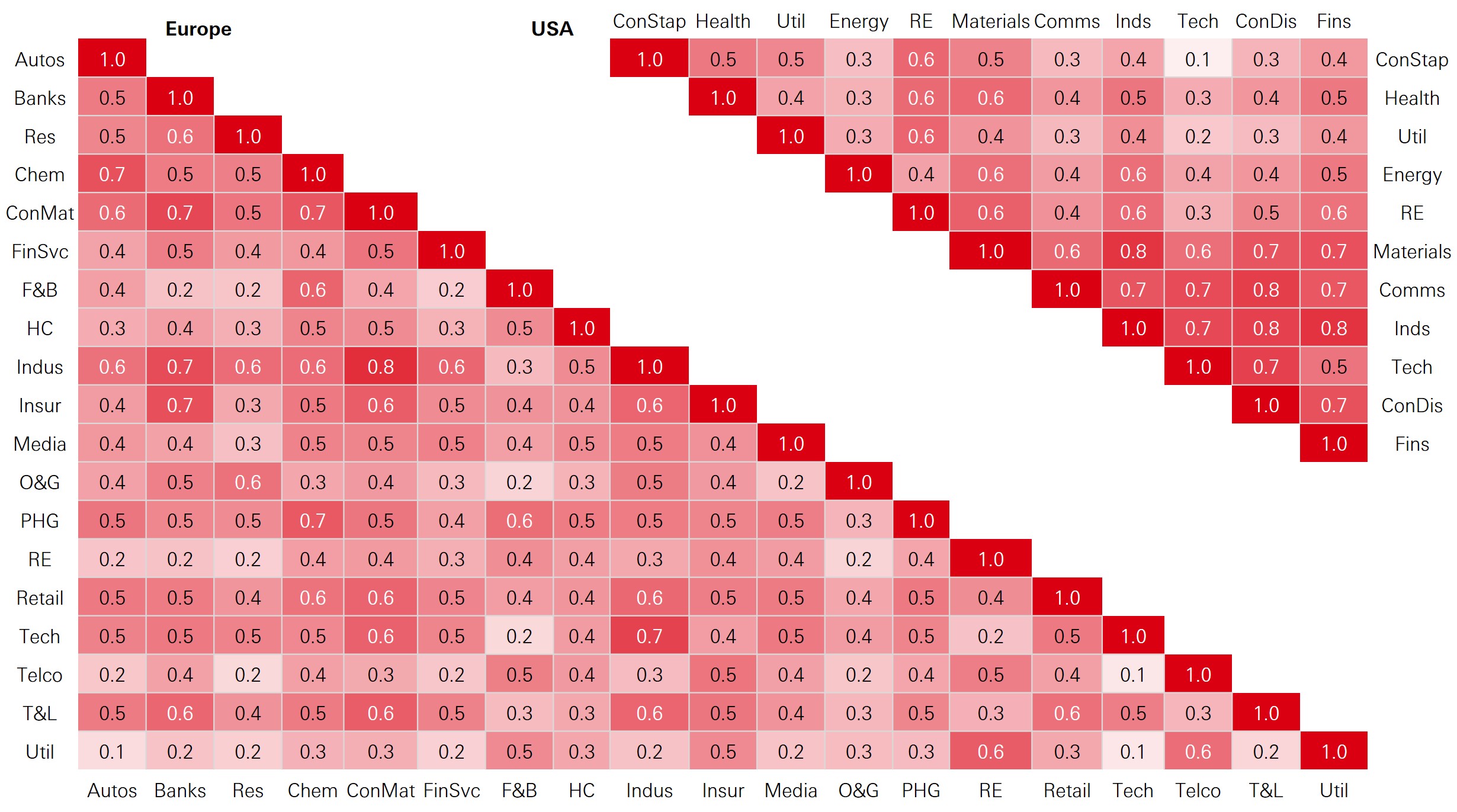

Finding diversification within equities has become an increasing point of focus for investors as rising index concentration has increased equity risk, particularly in the US where mega‑cap tech stocks have surged. The top 10 stocks now account for an elevated share of returns, making downside risks more asymmetric if leadership reverses.

At the same time, cross‑country equity correlations have risen. Once a popular avenue for diversification, most major regional pairs now exhibit correlations in the 0.6-0.8 range, suggesting that global macro policy and liquidity conditions increasingly dominate local drivers. This reduces the diversification value of simple regional allocation.

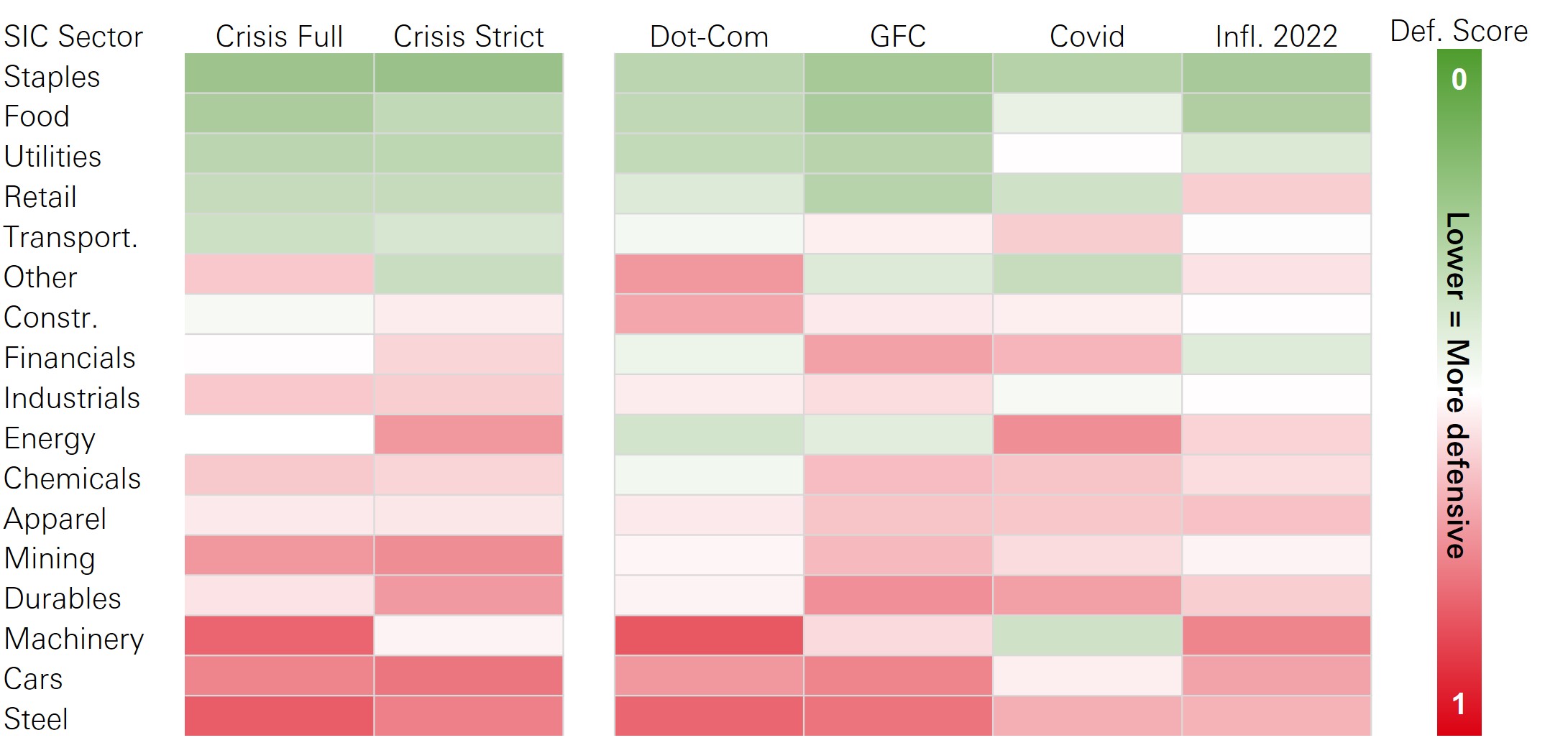

Instead, cross-sector correlations display a much broader range of correlation metrics, with sectors such as utilities, telecoms and consumer staples displaying defensive qualities. Further sector analysis using Fama–French industry portfolios shows that defensive leadership is persistent, but downside sensitivity is regime dependent. A good illustration of this is the performance of food and utilities during the Covid pandemic.

Figure 4: Cross-sector correlations display route to equity diversification

Click the image to enlarge

Source: Bloomberg as of March 2026. Note: The correlation is for the last 24 months.

Figure 5: Traditional defensives are consistently more resilient across stress episodes

Source: Eugene F. Fama and Kenneth R. French, Bloomberg as of March 2026. Note: “Crisis Full” represents a broad stress regime capturing the full market event (build-up, drawdown and recovery), providing more observations and more stable defensive metrics. “Crisis Strict” represents a narrower, high-intensity window isolating the peak stress phase, resulting in fewer observations. Dot-com period: 1 Jan 1998–31 Dec 2002. “Now” period: 1 Jan 2021–present. Block for Block-bootstrap had size of 6M.

Factor behaviour adds further nuance. In the US, returns remain heavily influenced by momentum and large‑cap leadership, consistent with narrow index breadth. The value factor has been cyclical – lagging in growth‑dominant, momentum‑heavy phases, but stabilising as macro dispersion and rate volatility increase. Outside the US, value performance has been more stable in Europe, the UK and emerging markets, reflecting different sector mixes and lower exposure to US‑style mega‑cap technology.

FX and commodities in a fragmenting world

Currencies and commodities have long provided important safe haven candidates, but their hedging roles are being reshaped by geopolitical fragmentation, fiscal trajectories and evolving central bank action.

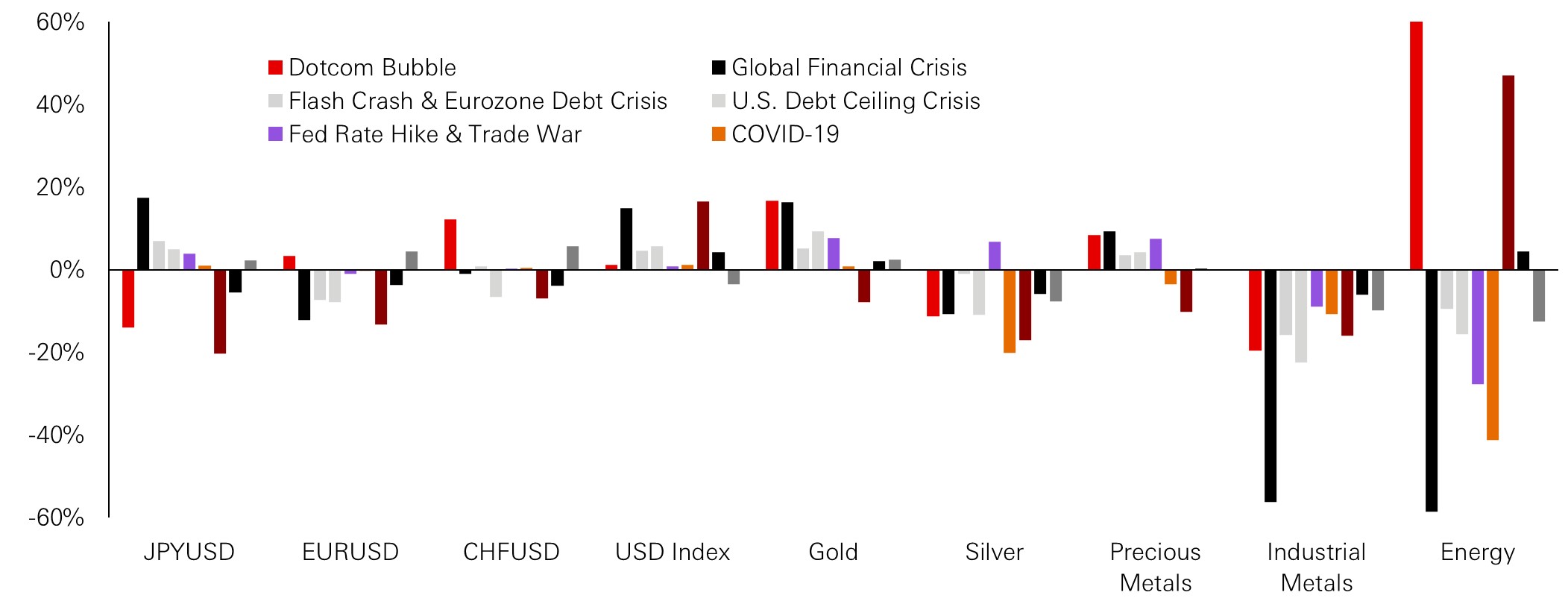

Historically, the US dollar, Swiss franc and gold have been among the assets most frequently providing protection during equity drawdowns. Analysing past crises including the global financial crisis, Covid‑19 and recent geopolitical shocks confirms that these assets have often delivered positive returns when equities sold off, although notable exceptions highlight the conditional nature of their safe haven status.

Figure 6: Performance during major historical risk-off events

Click the image to enlarge

Source: HSBC Asset Management, Bloomberg, February 2026. Periods were defined as: Dotcom Bubble: Apr. 2000 - Sep. 2002, Global Financial Crisis: Nov. 2007 - Feb. 2009, Flash Crash & Eurozone Debt Crisis: May. 2010 - Jun. 2010, U.S. Debt Ceiling Crisis: Jul. 2011 - Sep. 2011, Fed Rate Hike & Trade War: Oct. 2018 - Dec. 2018, Covid-19: Feb. 2020 - Mar. 2020, Ukraine War: Jan. 2022 - Sep. 2022, Bond Market Rout & Recession Fears: Aug. 2023 - Oct. 2023, Liberation Day: Mar. 2025 - Mid Apr. 2025.

The US dollar depreciated sharply in 2025, despite heightened volatility, as aggressive tariffs and debates over Federal Reserve independence eroded confidence, prompting some investors to reduce exposure to US Treasuries. However, during the current episode of tensions in the Middle East, the dollar’s behaviour reverted toward a more traditional safe haven asset, illustrating how political and institutional factors can temporarily override standard risk‑off patterns.

The Swiss franc continues to display classic safe haven characteristics, but its small market size limits its capacity to absorb large global flows. The Japanese yen, meanwhile, transitioned into a more counter‑cyclical currency after 2005, when net foreign income began to exceed the trade surplus, but it remains vulnerable to oil price spikes due to Japan’s net energy importer status.

On the commodity side, gold has evolved from a passive inflation hedge into a strategic competitor to US Treasuries as a reserve asset, particularly for non‑Western central banks seeking sanction resistant assets with zero counterparty risk. At the same time, gold’s short‑term performance remains sensitive to real yields, positioning and technical factors; for example, during the early phase of the Ukraine war, rising real yields weighed on gold despite elevated geopolitical risk. More recently, gold has failed to provide an effective hedge during the current Middle East conflict after its strong run in 2025 and early 2026 meant that it was overvalued coming into the volatility.

Energy prices are generally not an equity hedge, apart from in certain circumstances where geopolitical tensions are centred on oil‑producing regions and supply fears dominate.

Using options for diversification

Options can be used to gain exposure to volatility, particularly through long (equity) option positions that typically benefit from rising implied volatility and negative equity returns during drawdowns. Equity sell-offs are often accompanied by volatility spikes and rising cross-asset correlations, which can weaken traditional diversification. In such regimes, long-volatility option overlays may provide a more defensive, convex return profile.

Options markets are usually accessible during sell-offs, although bid–ask spreads can widen and execution costs can rise. A wide range of strikes and maturities allows payoff profiles to be tailored to specific risks.

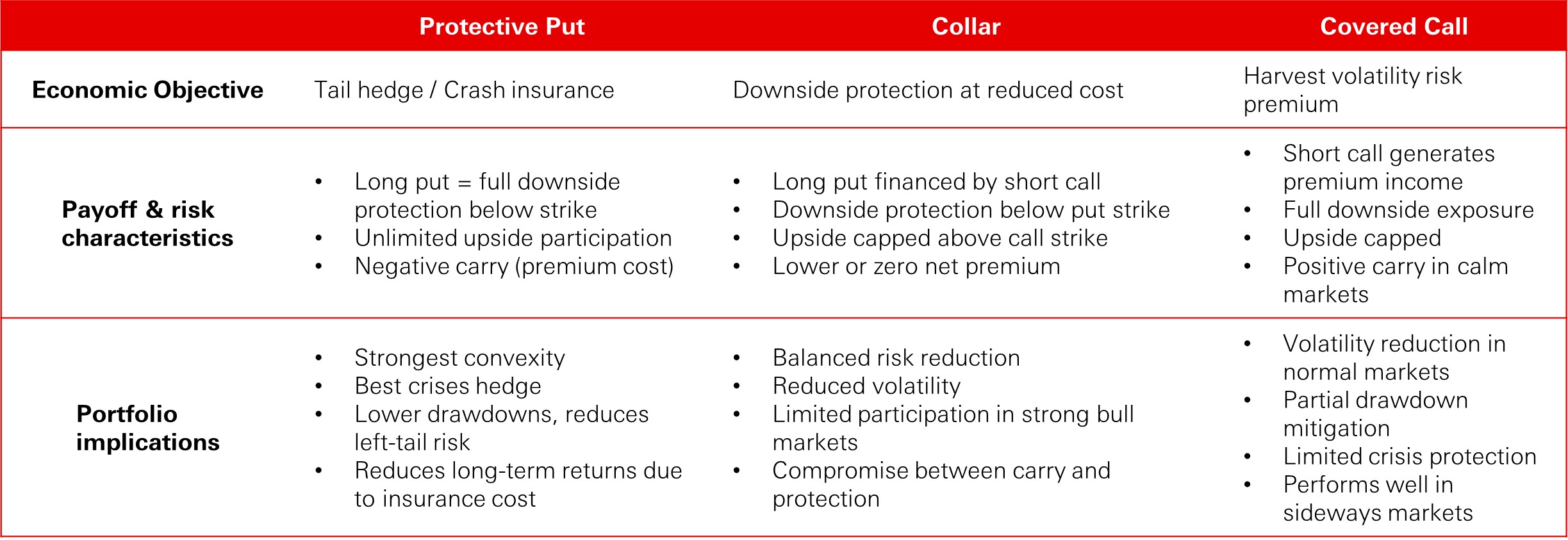

Figure 7: Option based strategies as safe havens and reliable diversifiers

Click the image to enlarge

Source: HSBC Asset Management, March 2026.

Long-term benchmark evidence for protective put, collar and covered call strategies suggest that option overlays can reduce maximum drawdowns relative to unhedged equity exposure, but outcomes depend materially on implementation choices (strike, tenor, roll rules) and transaction costs, and they typically reduce upside participation in strong bull markets.

Protective puts tend to offer the strongest crisis protection; collars provide more balanced risk reduction by partially funding the hedge; and covered calls are short volatility strategies that monetise volatility risk premia but generally provide only limited drawdown protection.

Importantly, no single options strategy dominates across all environments; the choice between long‑ and short‑volatility structures depends on expectations about crisis frequency and severity, the level of implied volatility and tolerance for carry costs versus drawdowns. However, they can play a structural role in tail-risk management, particularly when traditional hedges such as bonds, FX or commodities are less reliable.

Dynamic, regime‑based hedging

Across fixed income, equities, FX, commodities and options, the evidence points to a common conclusion: safe‑haven behaviour is highly regime‑dependent rather than fixed. Hedging characteristics have varied with growth-inflation dynamics, the origin of shocks, policy responses, fiscal conditions and market structure, so assets that appeared defensive in one episode have not always played the same role in the next.

Historical crises and the recent experience of 2025–26 illustrate this point clearly: nominal sovereign bonds, traditional safe‑haven currencies, gold, defensive equity sectors and option strategies have each provided material diversification benefits in some environments, yet all have also faced periods when their protective qualities were weaker or briefly reversed. Taken together, this suggests that no single static hedge works across all macro and market regimes, and that effective diversification may call for a more dynamic approach.

Continue reading:

Emerging markets: Beyond dollar luck

Source: HSBC Asset Management, May 2026. The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target where provided is indicative only and not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecast, projection or target.

Important information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agengy;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327)

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D070196_V2.0; Expiry date: 30.04.2027.